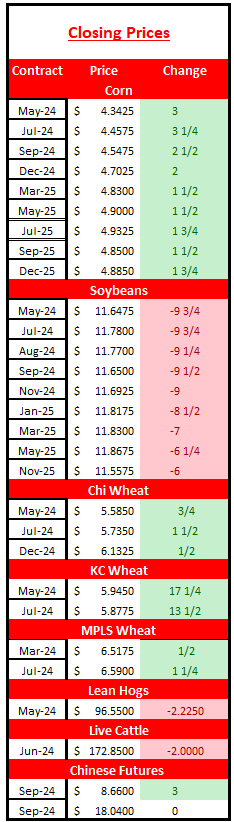

Another choppy day of trading, with mixed results. May corn came a penny shy of regaining back all of yesterday’s loss. May corn closed 3 cents higher, with December futures up 2 cents. Soybeans traded higher overnight, but sizzled during the day session and closed near 4 week lows. May beans closed 16 cents off session highs, and 9 3/4 cents lower for the day. The November contract finished the day 9 cents lower, as well. Wheat prices climbed higher, with KC finishing near the highs of the day. Nearby CBOT wheat closed 3/4 cents higher, KC up 17 and MPLS settled up 1/4 cent.

The big action of the day occurred in the outside markets. According to the latest consumer inflation reading, inflation is very much alive. March inflation was pegged at 3.5%, up from February’s 3.2% rate. A reduction in interest rates will now likely have to wait until September. There is even discussion of a possible increase in interest rates if inflation rises further. Yikes. Upon the release of the report, the Dow fell like a rock. The Dow lost 422 points on the day, marking the 3rd straight session of losses. Gold fell $10 to $2,352 and oil rose $1 to $86.25/barrel.

The dollar index moved over a full point higher today. That is a huge move. And, one that hurts our competitiveness in the export market. As you can see in the chart below, the dollar has been trending upward since mid January.

News was on the light side today. The USDA reported a 9.3 mbu new crop soybean sale to Unknown this morning. But, that didn’t do much to move the needle in new crop bean futures. Ethanol output fell 17K bpd this past week to 1.056 mbpd. While it was a disappointment to see a drop in production, today’s number is still better than the 5 week average. Stocks fell, which is a positive. We expect the USDA to make a few revisions in demand in tomorrow’s report.

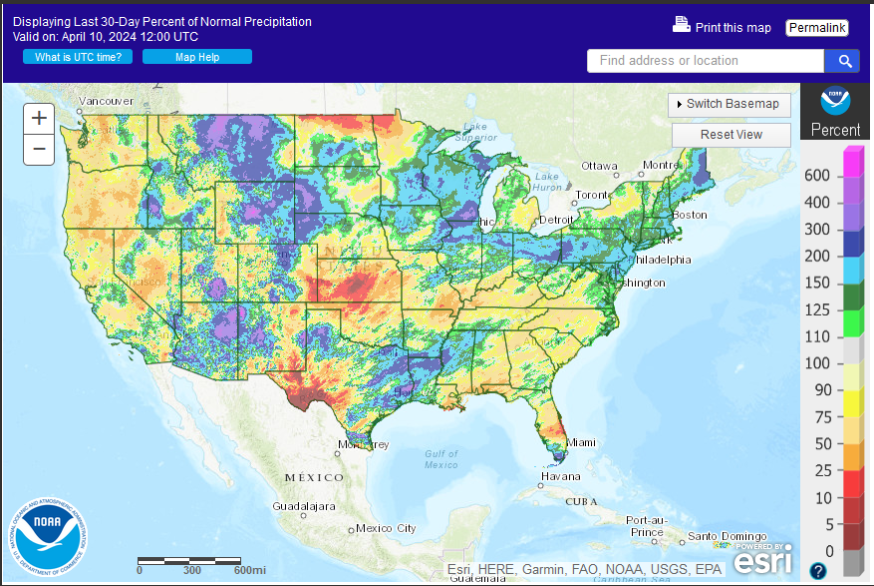

The map below shows precipitation in the last 30 days as a percent of normal. As, per usual, it is too wet for some and too dry for others. KC wheat futures were up double digits today, as traders added a weather premium to the dry start in the Southern Plains.

Eric Snodgrass (Nutrien Ag Solutions) recently commented – “If you told me to pin down where I think the drought risk could be,” he says, “My assessment as of early April is going to tell you to watch the Southern plains, the mid-South, the Delta region, or the Southeast. In other words, the Cotton Belt, not the Corn Belt.” He tells Brownfield historical data shows La Nina is typically favorable for the Corn Belt… “What that often gives us is a warmer, hotter summer than average, but a stormier summer than average across the Corn Belt.” He says, “So, it’s one of those odd years where we’re warm and wet, not cool and wet, or warm and dry.” Snodgrass says the uncertainty lies in the timing…

First things first. We have to get the crop planted before we worry about the growing season. Of most immediate concern are the nearby forecasts, as it isn’t looking very promising for planting much of anything in the ECB for the next couple of weeks. But, it is too early to get excited about planting delays on April 10th. May 10th is another story.

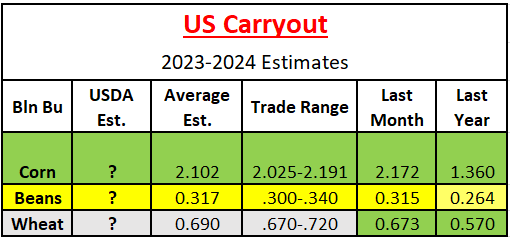

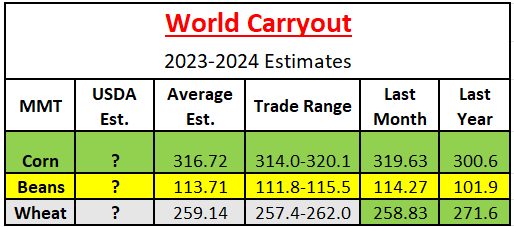

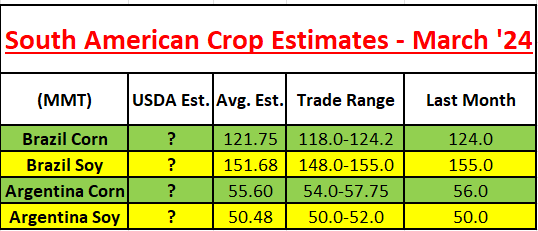

The USDA April report will be released tomorrow at 11 am CDT (CBOT time).

Good Night.

Disclaimer: This material should be construed as market commentary, merely observing economic, political and/or market conditions, and not intended to refer to any particular trading strategy, promotional element or quality of service provided by AgriSource Inc. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. These materials represent the opinions and viewpoints of the author, and do not necessarily reflect the viewpoints and trading strategies employed by AgriSource, Inc.

AgriSource, Inc. is not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. It does not constitute an individualized recommendation, or take into account the particular trading objectives, financial situations, or needs of individual customers. Contact AgriSource, Inc. designated personnel for specific trading advice to meet your trading preferences or goals.