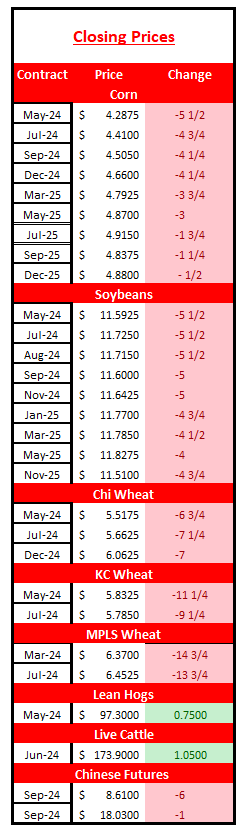

Prices finished lower today in response to today’s USDA report. Carryouts increased more than expected for soybeans and wheat, and corn carryout didn’t fall as much as the trade expected. 3 for 3, with the Bulls on the wrong side. Corn prices closed near session lows. May corn settled 5 1/2 cents lower with new crop down 4 cents. Soybeans finished a nickel lower, with May closing 8 cents off session lows. Nearby CBOT wheat closed nearly 7 cents lower, KC down 11 and MPLS fell 15 cents.

The outside markets fared better than yesterday. The government released the PPI and core PPI reports today, with something for everyone. The Dow traded back and forth, and ultimately finished the day nearly unchanged. Gold had a big day – up nearly $40. The dollar index was slightly lower, and oil was .60 cents lower.

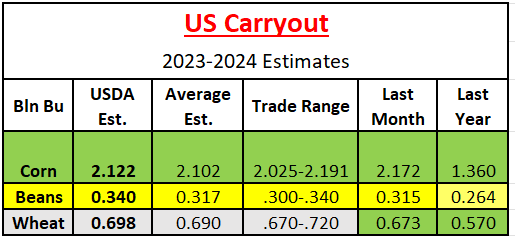

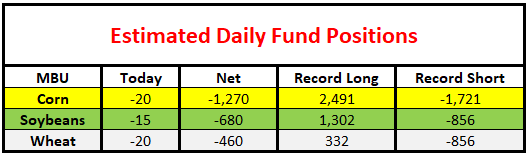

Today’s report didn’t favor the Bulls, but it wasn’t a real game changer either. In a nutshell, corn carryout fell 50 million bushels, but the market was expecting a bigger cut given the Stocks report. The USDA increased both ethanol and feed usage 25 mbu each, in today’s report. Traders were disappointed with today’s numbers, but expect the USDA to continue to trim carryout in future reports. Be patient.

The soybean guess was a big miss – to the tune of 23 mbu. The USDA revised exports 20 mbu lower, lowered imports 5 million and dropped seed and residual a combined 11 million. All told, carryout increased 25 million when the trade was expecting only a 2 million increase.

The wheat numbers were not much of surprise. The USDA lowered imports 5 mbu and feed use 30 mbu, resulting in a 25 mbu increase in ending stocks.

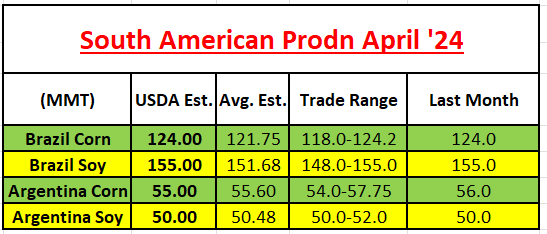

In addition to the increase in US stocks, the USDA barely made any changes to the South American crop. The USDA only made a minor cut of 1 mmt (55 mmt) to the Argentina corn crop from last month. Big deal.

There is quite a disparity between the USDA and Rosario corn estimates. Rosario came out today and lowered the Argentina corn crop from 57.0 mmt to 50.5 mmt due to unprecedented damage due to leafhoppers. USDA thinks its an isolated problem, Rosario (USDA of Argentina) does not. Leaf hoppers are very small, and have piercing and sucking mouth parts. They can cause damage to plants by sucking the plant sap from leaves and growing shoots. Rosario commented that there may be more damage.

The USDA estimates for Brazil are also much higher than CONAB (USDA version in Brazil). USDA is projecting a 124 mmt corn crop but CONAB is estimating 110.9 mmt. USDA is pegging the Brazilian bean crop at 155 mmt, but CONAB is at 146.5. There are a couple of reasons that may explain why USDA numbers are so high. The USDA doesn’t like to make big changes this early in the season, and secondly, the USDA is using a larger acre base. It will be interesting to see final production numbers once harvested. Someone is wrong.

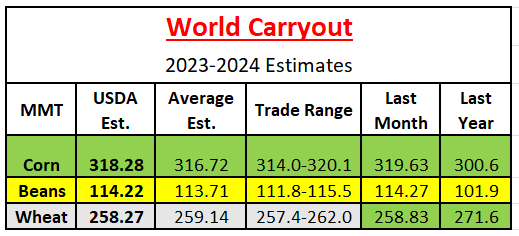

Only minor changes in the world balance sheets. Larger carryouts vs last year for corn and soybeans.

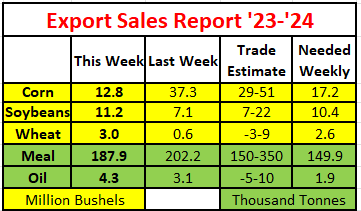

The USDA released the Export Sales report early in the day. Corn sales hit a marketing year low, with soybean and wheat sales neutral. Chatter is that China is/has cancelled 11.8 mbu of Ukraine corn for April and May shipment. Some think China is cancelling sales to prop up prices for their farmers. Or, maybe they are waiting to score a bargain from Brazil?

The USDA released the Export Sales report early in the day. Corn sales hit a marketing year low, with soybean and wheat sales neutral. Chatter is that China is/has cancelled 11.8 mbu of Ukraine corn for April and May shipment. Some think China is cancelling sales to prop up prices for their farmers. Or, maybe they are waiting to score a bargain from Brazil?

Today’s action was certainly disappointing. May corn continues to bang around in the range of $4.25-4.45. Today’s report didn’t change anything. May soybeans hit $11.51 at the low today and bounced back. That is a positive, but prices are going to fight to get back to $12.

Good Night.

Disclaimer: This material should be construed as market commentary, merely observing economic, political and/or market conditions, and not intended to refer to any particular trading strategy, promotional element or quality of service provided by AgriSource Inc. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. These materials represent the opinions and viewpoints of the author, and do not necessarily reflect the viewpoints and trading strategies employed by AgriSource, Inc.

AgriSource, Inc. is not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. It does not constitute an individualized recommendation, or take into account the particular trading objectives, financial situations, or needs of individual customers. Contact AgriSource, Inc. designated personnel for specific trading advice to meet your trading preferences or goals.